Millennials think they are worse off than their parents, but, maybe, a shift in the labour market and digital connectivity has given them a hidden advantage

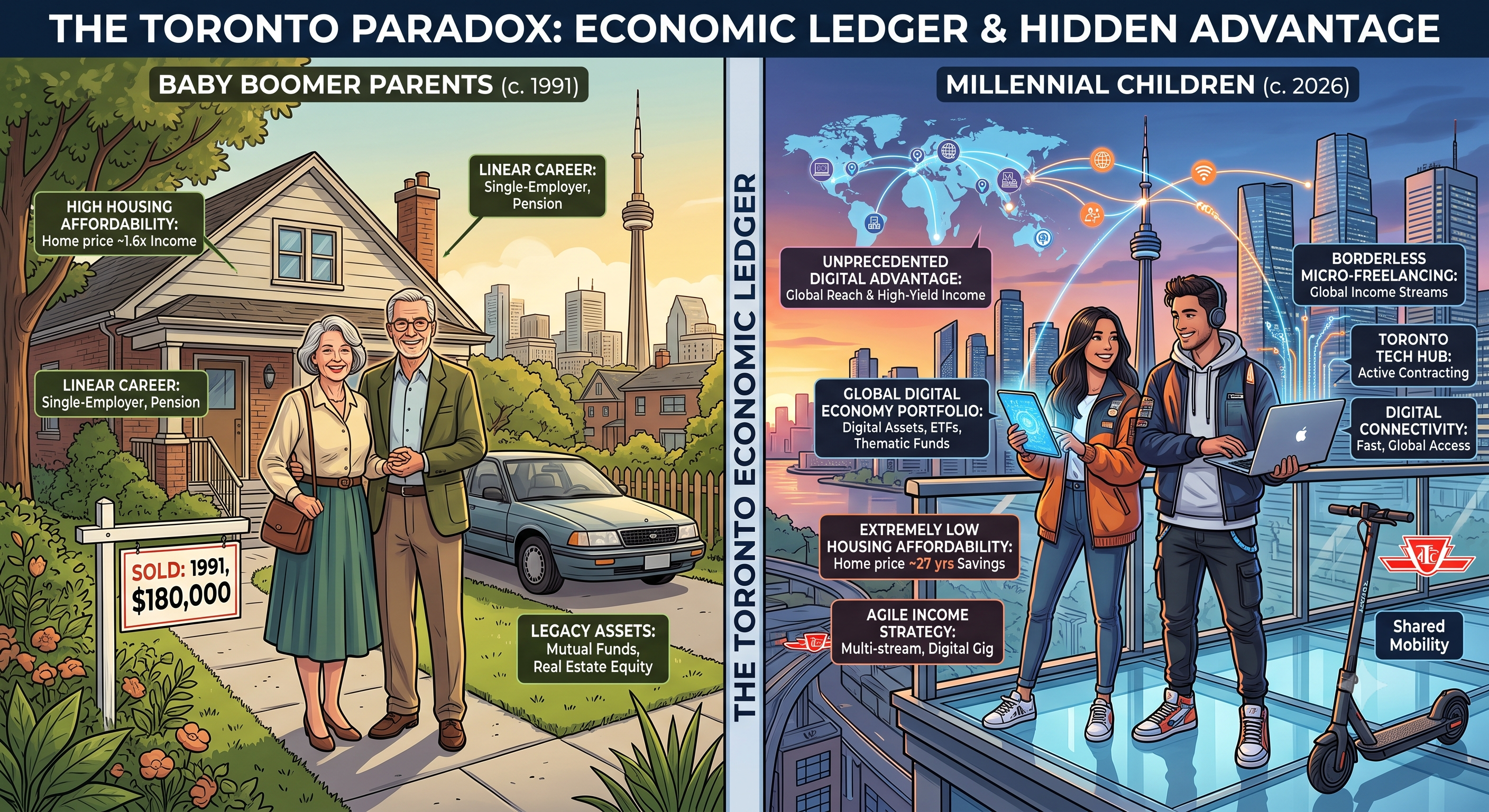

The financial narrative of Toronto Millennials is a stark paradox. By traditional metrics—namely housing affordability, debt-to-income loads, and legacy asset accumulation—they are undeniably worse off than their Baby Boomer parents. However, a profound structural shift toward a globalized, digital knowledge economy has granted them a "hidden advantage." Unprecedented digital connectivity, borderless micro-freelancing, and Toronto's emergence as a premier global tech hub allow modern workers to bypass traditional corporate bottlenecks and access high-yielding, agile income streams that were entirely unavailable to previous generations.

The Traditional Economic Ledger: Where Millennials Fall Behind

Evaluating the financial health of Millennials in the Greater Toronto Area (GTA) through the traditional lenses of homeownership and debt insulation reveals severe systemic disadvantages relative to the Baby Boomer generation at the same life stage.

The Real Estate Chasm

For Baby Boomers, housing was a stable vehicle for wealth generation. In the 1980s and early 1990s, a standard home in Toronto cost roughly 1.6 times the average annual family income [1]. Today, systemic supply imbalances and asset inflation have completely decoupled home prices from local wages.

A landmark 2026 Statistics Canada report highlights the domestic fallout of this crisis:

-

Delayed Launch: In Toronto, 26.1% of Millennials (aged 25 to 39) live with at least one parent, compared to a baseline of just 8.2% for Baby Boomers nationwide in 1991 [1:1][2]. For the youngest cohort of Toronto Millennials (aged 25 to 29), that number climbs to nearly one in two (48.6%) [1:2].

-

The Shrinking Detached Dream: The homeownership rate for Millennials sits at 49.9%, compared to 55.9% for Boomers in 1991 [1:3]. More tellingly, the type of real estate acquired has degraded. In Toronto, the proportion of young homeowners holding a single-detached home plummeted from 32.7% in 1991 to just 19.4% in 2021 [1:4].

-

The Down Payment Mountain: Across the GTA, it now takes an estimated 27 years of average savings to accumulate a down payment on a standard residential property, driven by home prices soaring over 300% since 2000 against a broader inflation rate of only 48% [1:5].

Staggering Debt-to-Income Loads

While Canadian Millennials technically earn higher inflation-adjusted median household incomes than Boomers did at the same age ($44,093 vs. $33,350) [3], their financial cushions are razor-thin due to liabilities:

-

Educational Leverage: To remain competitive in Toronto’s knowledge economy, roughly three-quarters of Millennials pursued post-secondary education, compared to just over half of Gen X and far fewer Boomers, saddling them with significant upfront student debt [3:1].

-

Leveraged Assets: Millennial mortgage principals are over 2.5 times larger relative to income compared to previous generations [3:2]. Households headed by individuals aged 35 to 44 carry a crushing debt-to-disposable income ratio of 245.8%, leaving them highly vulnerable to economic and labor market shocks [4][5].

The Hidden Advantage: Structural Shifts and Digital Connectivity

Despite the bleak real estate reality, viewing Millennials solely as an economically depressed generation ignores a massive structural evolution in how wealth, career equity, and daily utility are generated.

| Economic Vector | Baby Boomer Generation (c. 1991) | Millennial Generation (c. 2026) |

|---|---|---|

| Living with Parents (Toronto) | ~8.2% (National average) [1:6] | 26.1% [1:7] |

| Toronto Detached Homeownership | 32.7% [1:8] | 19.4% [1:9] |

| Primary Economic Engine | Local/Regional Corporate & Manufacturing | Global Digital Ecosystem & Specialized Tech [6] |

| Income Strategy | Rigid, single-employer linear ladder | Agile, multi-stream, borderless freelancing [7] |

| Investment Framework | Legacy equities, mutual funds, real estate | Programmatic robo-advisors, digital/thematic assets [8] |

The Borderless Knowledge Economy

Baby Boomers were largely bound to the regional constraints of the Toronto labor market. If local enterprises downsized, their options were strictly geographically limited.

In contrast, Millennials utilize digital connectivity to separate active earning potential from local geometric boundaries:

-

The Tech Hub Premium: Toronto has evolved into North America’s fastest-growing technology ecosystem. Self-employed tech professionals and independent digital contractors now make up 23% of Toronto's entire tech workforce [6:1].

-

Micro-Freelancing & Global Arbitrage: Armed with digital infrastructure, Toronto's white-collar Millennials have embraced hyper-specialized micro-freelancing (e.g., localized translation, machine learning engineering, programmatic ad management). By shifting away from standard local retail or corporate entry roles, they can source premium contract fees globally via digital platforms, effectively cutting out regional corporate middlemen [7:1].

Because real estate acquisition is delayed, many Toronto Millennials operate on an "asset-light" financial model. Rather than sinking capital into heavy property maintenance, illiquid down payments, and high-interest mortgages, un-landed Millennials maintain resilient levels of consumption and reallocate capital into alternative, high-growth investment engines.

Advanced Financial Ecosystems

The integration of digital technology into financial infrastructure has changed wealth management optimization:

-

Algorithmic and Programmatic Wealth: Millennials are fundamentally different investors than their parents. Over 67% utilize computer-generated robo-recommendations and automated micro-investing platforms as the core of their strategies [8:1].

-

Diversification Beyond Housing: While Boomers relied almost entirely on primary residential growth to build net worth, youngest-bracket households (<35) expanded their net worth in recent cycles at an above-average pace (+5.7%) primarily driven by a 12.2% surge in liquid financial assets, including global growth equities, decentralized digital assets, and thematic future-focused ETFs [5:1][9].

The Intragenerational Divide: A Bifurcated Generation

The final verdict on whether Toronto Millennials are truly worse off depends heavily on an unprecedented internal polarization within the cohort itself.

Over the next two decades, Canada is undergoing the largest intergenerational wealth transfer in its history, moving over $1 trillion from aging Baby Boomers to Millennial and Gen Z heirs [9:1].

This creates two distinct classes of Millennials in Toronto:

-

The Inherited Asset Class: Millennials who leverage familial equity to secure property down payments, or who stand to inherit properties in Toronto's multi-million dollar residential market. These individuals couple high digital earning capacity with legacy asset protection, making them the wealthiest generation in Canadian history [3:3].

-

The Isolated Renter Class: Millennials lacking intergenerational safety nets who are forced to contend with an unforgiving local rental market. For this demographic, despite superior digital skills and high nominal wages, a massive portion of their disposable income is eaten up by local cost-of-living constraints [1:10][5:2].

Ultimately, Toronto Millennials possess a massive, hidden structural advantage in how they work, adapt, and build modern enterprises globally. However, this digital leverage acts as an equalizer rather than a total victory, helping them navigate an urban landscape that is fundamentally more expensive and volatile than the one their parents experienced.

The Hub. (2026). Canadian Millennials living with parents into adulthood double the rate of Boomers at same age. https://thehub.ca/2026/05/13/millennials-living-with-parents-into-adulthood-at-double-the-rate-of-boomers-at-same-age/ ↩︎ ↩︎ ↩︎ ↩︎ ↩︎ ↩︎ ↩︎ ↩︎ ↩︎ ↩︎ ↩︎

Statistics Canada. (2026). Millennials in the Canadian housing market: An intergenerational comparison. Government of Canada. https://www150.statcan.gc.ca/n1/pub/46-28-0001/2026001/article/00001-eng.htm ↩︎

CBC News. (2019/2026). Millennials earn more than their parents did — but owe a lot more. https://www.cbc.ca/news/business/millennials-income-statistics-canada-1.5106460 ↩︎ ↩︎ ↩︎ ↩︎

Global News. (2026). Twice as many millennials live with parents than boomers at their age. https://globalnews.ca/news/11837453/millennials-live-with-parents-boomers/ ↩︎

Statistics Canada. (2026). Distributions of household economic accounts for income, consumption, saving and wealth of Canadian households, fourth quarter 2025. Government of Canada. https://www150.statcan.gc.ca/n1/daily-quotidien/260413/dq260413a-eng.htm ↩︎ ↩︎ ↩︎

TechToronto & City of Toronto. (2016/2024). How Technology Is Changing Toronto Employment. https://www.toronto.ca/wp-content/uploads/2017/08/9585-TechTO_Report2016.pdf ↩︎ ↩︎

Toronto Business Journal. (2026). Gen Z and the Gig Economy: The Rise of Micro-Freelancing Among Toronto Students. https://www.tobj.ca/news/our_city/2026/07/02/35291-gen-z-and-the-gig-economy-the-rise-of-micro-freelancing-among-toronto-students.html ↩︎ ↩︎

TD Canada Trust. (2022/2025). How Do Different Generations Invest Money?. https://www.td.com/ca/en/personal-banking/advice/growing-money/how-different-generations-invest ↩︎ ↩︎

TD Asset Management. (2024/2026). Boomers, Millennials and the $1 Trillion Question. https://www.td.com/ca/en/asset-management/insights/blog/boomers-millennials ↩︎ ↩︎